May 6, 2025

Update: The UK supply figure has been updated from 0.19 to 0.14 sqm/capita to reflect net rather than gross rentable area, ensuring consistency with how other markets in the report are measured.

Market Overview

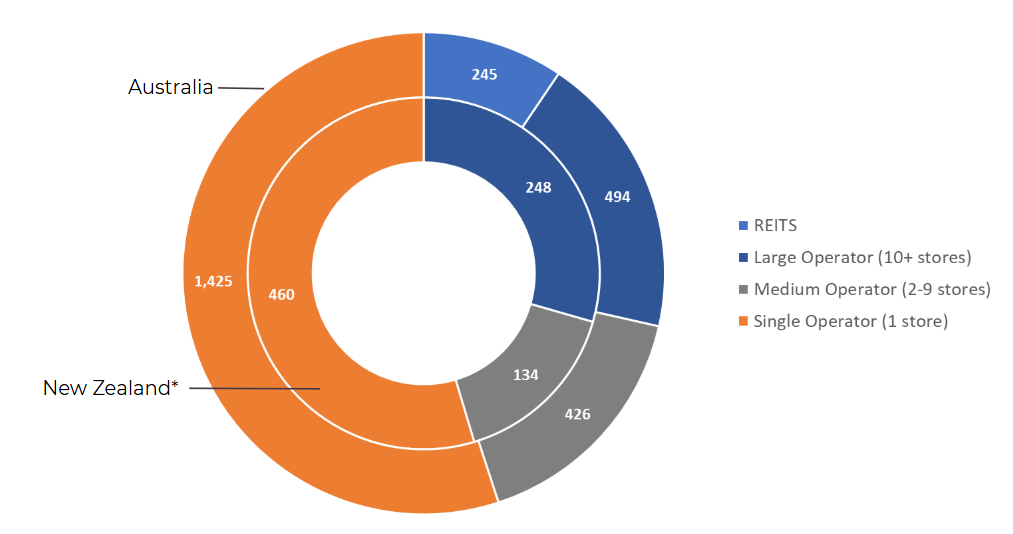

Accelerating demand, expanding use cases, and rising institutional interest are propelling the Australia–New Zealand self-storage sector into a new phase of growth. Together, the region is home to an estimated 3,432 facilities, with Australia accounting for nearly 2,590 and New Zealand for 842 – offering over 7.6 million square meters (sqm) of net rentable space. This a scale reflects both the market’s maturity and the increasing role storage plays in modern life.

Despite recent consolidation, the industry remains highly fragmented. REITs and large operators hold about 30% market share in each country, with mid-sized operators accounting for 16%. The remaining 54% of facilities are still operated by single-site operators – a structure that continues to attract investors seeking scale in a resilient asset class.

*While self-storage REITs such as National Storage REIT (NSR) and Abacus Storage King (ASK) are publicly listed on the Australian Securities Exchange, they are not classified as REITs in New Zealand due to differences in operational or organizational structures that do not meet the country’s REIT classification requirements.

Growth Drivers

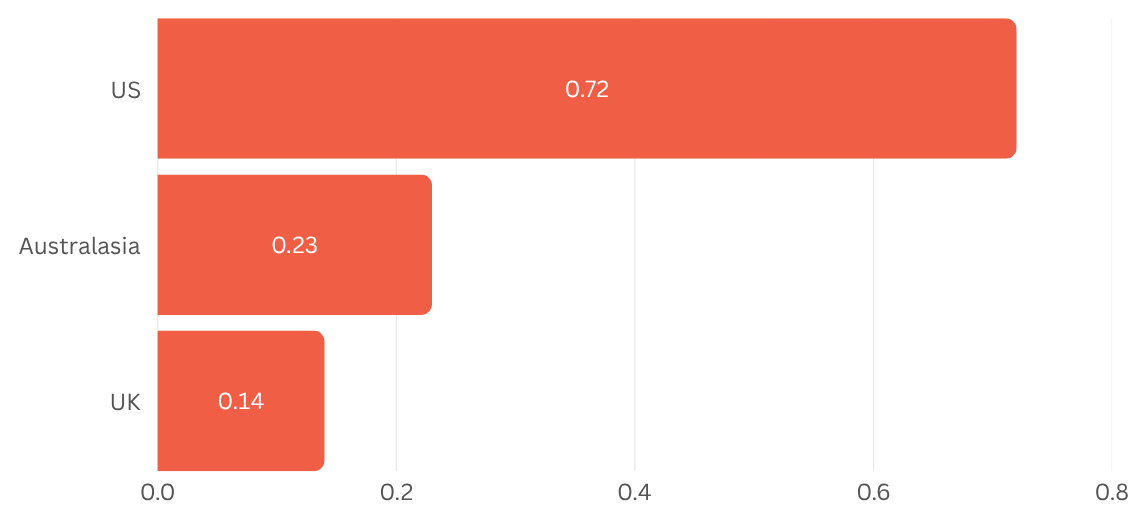

Compared to other major self-storage markets, Australasia’s supply sits at 0.23 sqm/capita, placing it between the more saturated U.S. market (0.72 sqm/capita) and the UK (0.14 sqm/capita). This relative undersupply highlights significant room for expansion and reinforces the region’s growing appeal as a global growth market for self-storage.

A convergence of demographic, economic, and lifestyle trends is propelling self-storage demand across Australia and New Zealand. Population growth, housing turnover, urban densification, and evolving lifestyles are intensifying pressure on available space. Simultaneously, the rise of e-commerce and ongoing supply chain challenges are prompting small businesses to seek flexible storage solutions amid escalating operating costs.

In Australia, an aging population is increasing demand as downsizing households require secure, accessible storage during life transitions. Labor shortages have also attracted many New Zealanders across the Tasman, further tightening housing markets in urban areas and boosting storage needs. Conversely, New Zealand’s population has recently surpassed 5.3 million, marking some of the fastest growth in the last decade, primarily driven by international migration . This surge, coupled with more frequent extreme weather events, is elevating demand for transitional and emergency storage solutions.

According to the Self Storage Association (SSA) of Australia, national occupancy averages around 87%, indicating strong user adoption and growing investor confidence. With these demographic shifts, migration patterns, and environmental factors converging, the self-storage sector in Australasia is well-positioned for sustained, long-term growth.

Pricing Trends

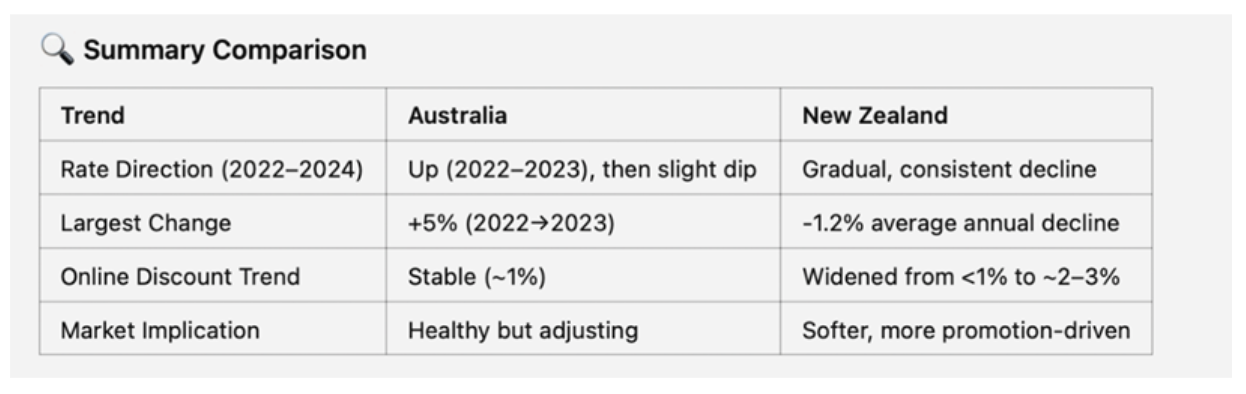

Like many major self-storage markets worldwide, Australia and New Zealand see peak leasing activity during the summer months, when demand is at its highest and pricing behavior is most revealing. To assess how pricing has evolved, peak rates for the most commonly rented unit – a 3×3 square meter- were compared annually from 2022 to the present. Interestingly, StorTrack data shows peak leasing occurs in January for Australia and late December for New Zealand. While both countries enter summer in December, this difference likely reflects school break schedules, with major life transitions – and storage demand – starting earlier in New Zealand. This subtle timing shift helps explain why pricing peaks sooner there, underscoring how local patterns influence national trends.

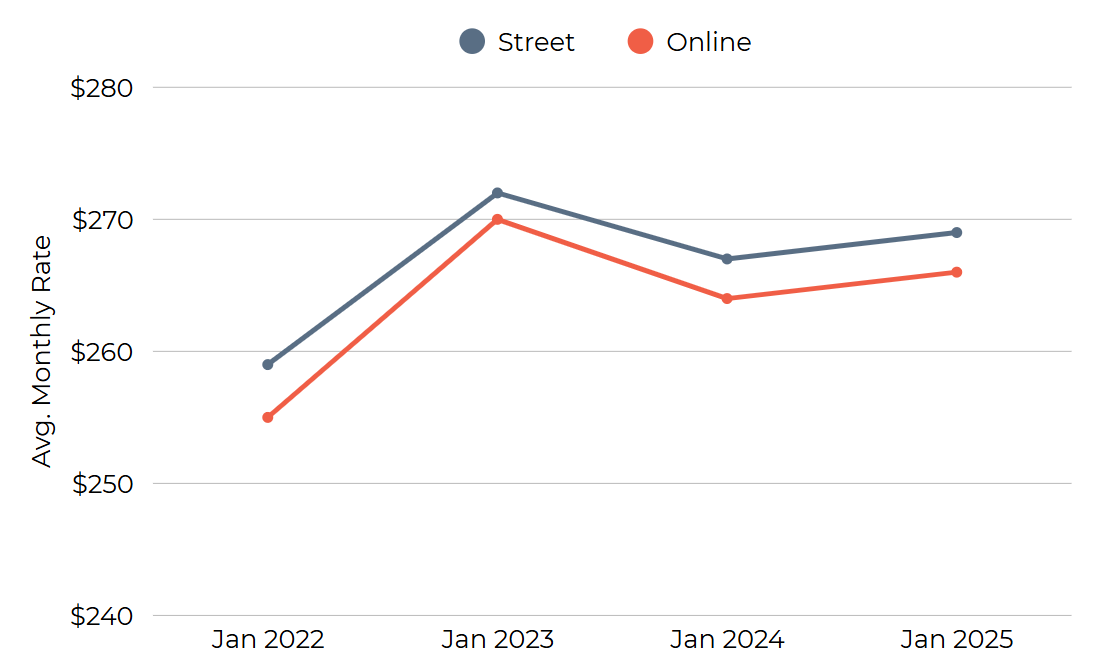

From 2022 to 2025, Australia’s self-storage market showed signs of solid yet fluctuating growth. The most notable increase occurred between 2022 and 2023, where average street rates for a 3×3 m² unit jumped by over 5%, rising from $258.54 to $272.21 AUD. This surge likely reflects a combination of post-COVID demand recovery, inflation, and stronger occupancy performance. However, the following year (2023 to 2024) saw a modest decline of 2% as rates dropped to $266.55 AUD, suggesting a market correction or increasing competition. Rates began to recover slightly in 2025, climbing to $269 AUD.

Online rates closely tracked street pricing throughout the period, maintaining a consistent discount of about 1%, indicating stable digital pricing strategies without heavy promotional swings. Overall, the market appears healthy, with short-term fluctuations tempered by long-term pricing discipline.

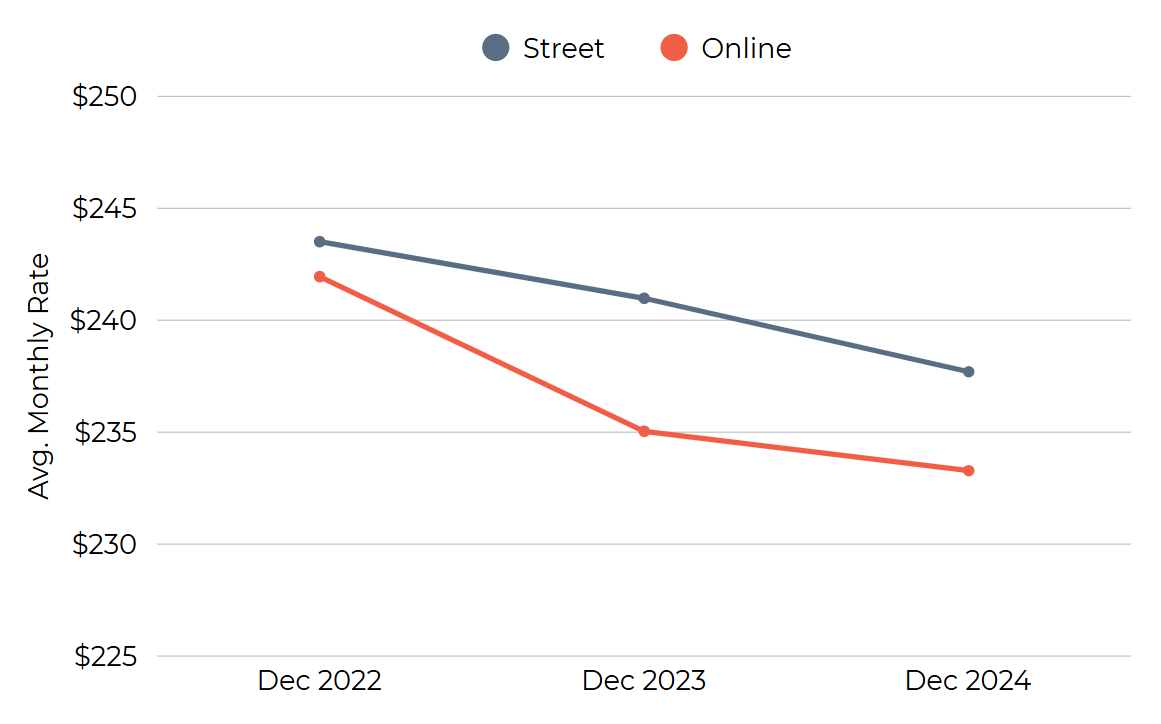

In contrast, New Zealand’s self-storage market has experienced a steady downward trend in peak season rates over the past three years. Average street rates declined from $243.51 AUD in 2022 to $237.70 AUD at the end of 2024, reflecting an average annual decrease of approximately 1.2%. This consistent softening suggests the market may be grappling with oversupply, weaker demand, or increased price competition. A more telling sign is the widening gap between street and online promotional rates: in 2022, the difference was minimal (just under 1%), but it expanded sharply to nearly 3% in 2023 before narrowing slightly to around 2% in 2024. This growing discounting behavior points to increasing reliance on promotions to attract tenants and fill vacancies.

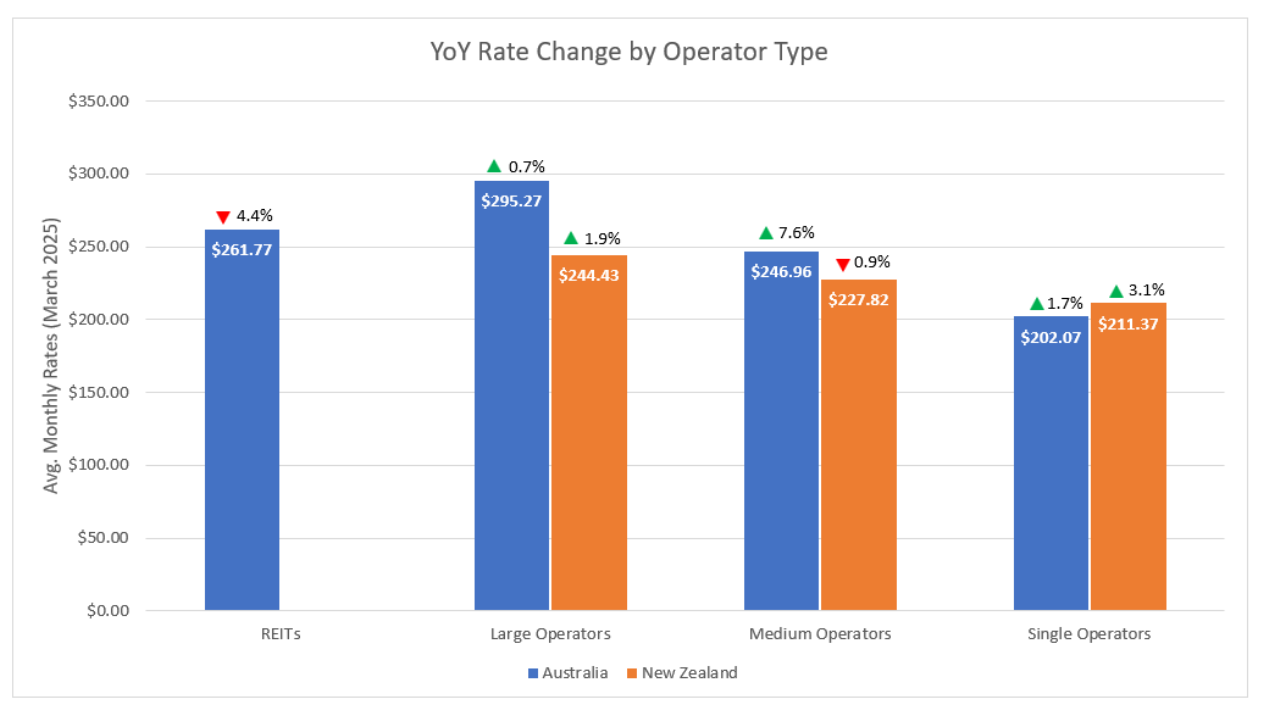

While peak rates offer a snapshot of pricing at the height of demand, a look at current average rates compared to the same period last year provides a pulse check on where the momentum is heading. As of April 2025, Australia’s average monthly rate remained steady at $266 AUD per square meter, though this stability masks notable shifts across operator types and regions.

Medium operators led the Australian market with 7.6% growth, signaling stronger pricing power and improved market positioning. Large operators posted modest gains, likely benefiting from operational scale and pricing consistency. In contrast, REITs saw a 4.4% decline, potentially reflecting rising competition or strategic price recalibrations. Meanwhile, single-location operators, while still offering the lowest rates, experienced steady growth, highlighting continued demand in this segment.

In New Zealand, large operators saw a year-over-year increase of nearly 2%, while medium operators experienced a slight decline – a stark contrast to the nearly 8% rate increase posted by the same segment in Australia. Interestingly, single operators in New Zealand outperformed their Australian counterparts, with average rates rising 3.1% over the past 12 months, signaling steady demand and pricing resilience among independents in the market.

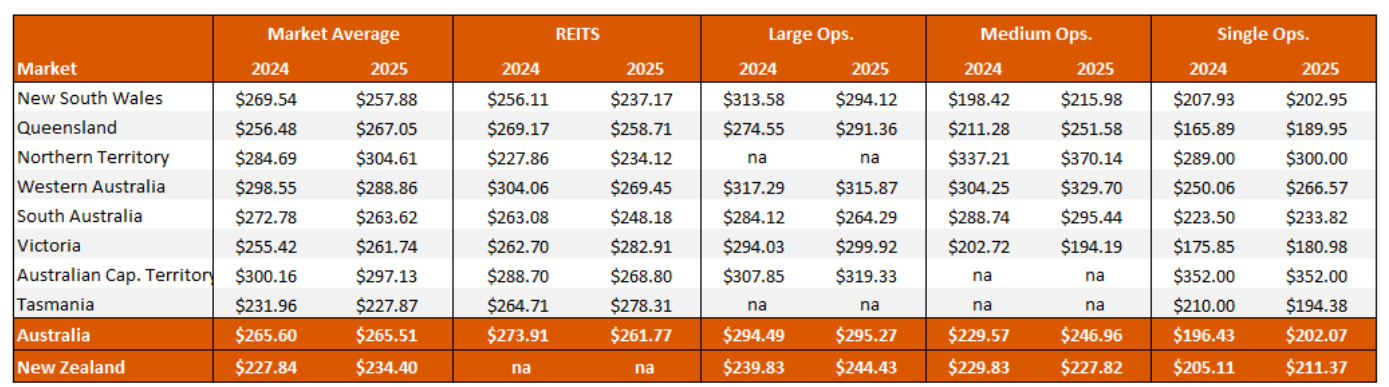

Regional Trends

A closer look at regional trends reveals patterns that national averages can obscure. Some areas show signs of oversupply, while others are tightening. Notably, Victoria and Queensland led in pricing growth across multiple operator types, likely driven by strong population inflows. In Western Australia, however, REITs posted sharp declines while medium operators raised rates, pointing to a shift in competitive dynamics within the region.

*In some states, pricing for certain categories is unavailable due to limited market presence or insufficient sample size.

Market Expansion & Investment

The self-storage sector in Australia and New Zealand continues to expand through a combination of acquisitions, institutional capital, and development. While high construction costs, limited land availability, and restrictive planning controls are slowing the pace of new supply, these constraints are helping to preserve occupancy levels and pricing strength in metro markets.

According to SSA Australia, there are over 250 projects under development in the region, representing a combined value of more than $2 billion—a clear indicator of long-term confidence in the sector.

KEY ACTIVITY HIGHLIGHTS

- GIC & NSR Joint Venture: Last year, Singapore’s GIC partnered with National Storage REIT (NSR) to launch a A$270 million fund that will support 10 self-storage construction projects across Australia over the next 12 to 18 months. GIC holds a 75% stake, while NSR manages the fund and retains 25% equity.

- NSR Pipeline Growth: By early 2025, NSR had completed 20 acquisitions and 7 developments, with 52 projects underway, reinforcing its dual strategy of roll-up growth and selective development.

- StorHub Expansion: During Q4 2024, StorHub acquired three Sydney facilities for A$110 million, adding over 18,000 sqm of NLA and nearly 2,000 units, expanding its national footprint to 11 sites valued at $420 million+

- SIA Development Fund: In late 2024, Storage Investment Australia (SIA) launched a $40 million fund targeting a $1 billion portfolio, focused on high-demand urban markets and long-term portfolio scale.

While new facility development remains measured due to planning and cost constraints, market consolidation is picking up pace, especially in New Zealand, where the potential sale of National Mini Storage – Auckland’s largest operator – could reshape the competitive landscape. The region’s highly fragmented sector continues to attract private equity, REITs, and institutional players seeking scale in a supply-constrained environment.

![]()

Self-storage continues to demonstrate its strength as a resilient asset class, offering steady income and pricing flexibility in a shifting economic landscape. Its short-term lease structure enables real-time rate adjustments—a key advantage in inflationary periods.

Investor interest remains strong. Storage Investment Australia (SIA) aims to grow its portfolio to $1 billion AUD over the next five years, while National Storage REIT (NSR) added seven new facilities in early 2025, expanding its portfolio to $5.1 billion AUD.

That said, near-term headwinds could temper growth. Geopolitical tensions and potential trade disruptions are fueling global uncertainty. In New Zealand, rising unemployment may weigh on household spending, even as inflation stabilizes in Australia. While monetary policy easing provides some relief, ongoing cost pressures and uneven recovery across sectors remain key risks.

Still, the long-term outlook is compelling. Urbanization, demographic shifts, and lifestyle changes continue to drive demand for flexible, space-efficient storage solutions. Operators that embrace data-driven pricing, prioritize customer experience, and pursue strategic expansion, whether through development or acquisition, will be best positioned to lead. Despite short-term volatility, the sector in both Australia and New Zealand is set for sustained, long-term growth.

![]()

StorTrack is the leading provider of self-storage market data and insights, enabling operators, investors, and developers to make informed, data-driven decisions. Since 2014, StorTrack has delivered accurate, actionable market analytics to self-storage professionals worldwide.

With coverage of over 3,400 self-storage facilities across Australia and New Zealand, StorTrack delivers critical market trends and rate data to the industry. Its powerful tools — including the Optimize platform, custom reports, and API — provide clear visibility into competitor pricing activity, automate reporting processes, and supply the data essential for effective rate optimisation, market feasibility assessments, and demand analysis.

Whether you’re refining pricing strategies, evaluating market opportunities, or growing your portfolio, StorTrack is your trusted partner for success in the self-storage sector across Australia, New Zealand, and beyond.