North America

North America UK

UK Europe

Europe Australia

Australia New Zealand

New ZealandMarket Overview

In December 2025, the UK and major EU self-storage markets continued to reflect an industry defined by low penetration, rising institutional maturity, and meaningful pricing power in urbanized regions. The UK remains Europe’s most developed self-storage market, with approximately 5,098 facilities and more than 116 million net rentable square feet of inventory, translating to roughly 1.74 square feet per capita. Average advertised pricing stood at £2.64, underscoring the UK’s position as the most established and liquid self-storage ecosystem in Europe, supported by deeper operator scale and consumer familiarity with the product.

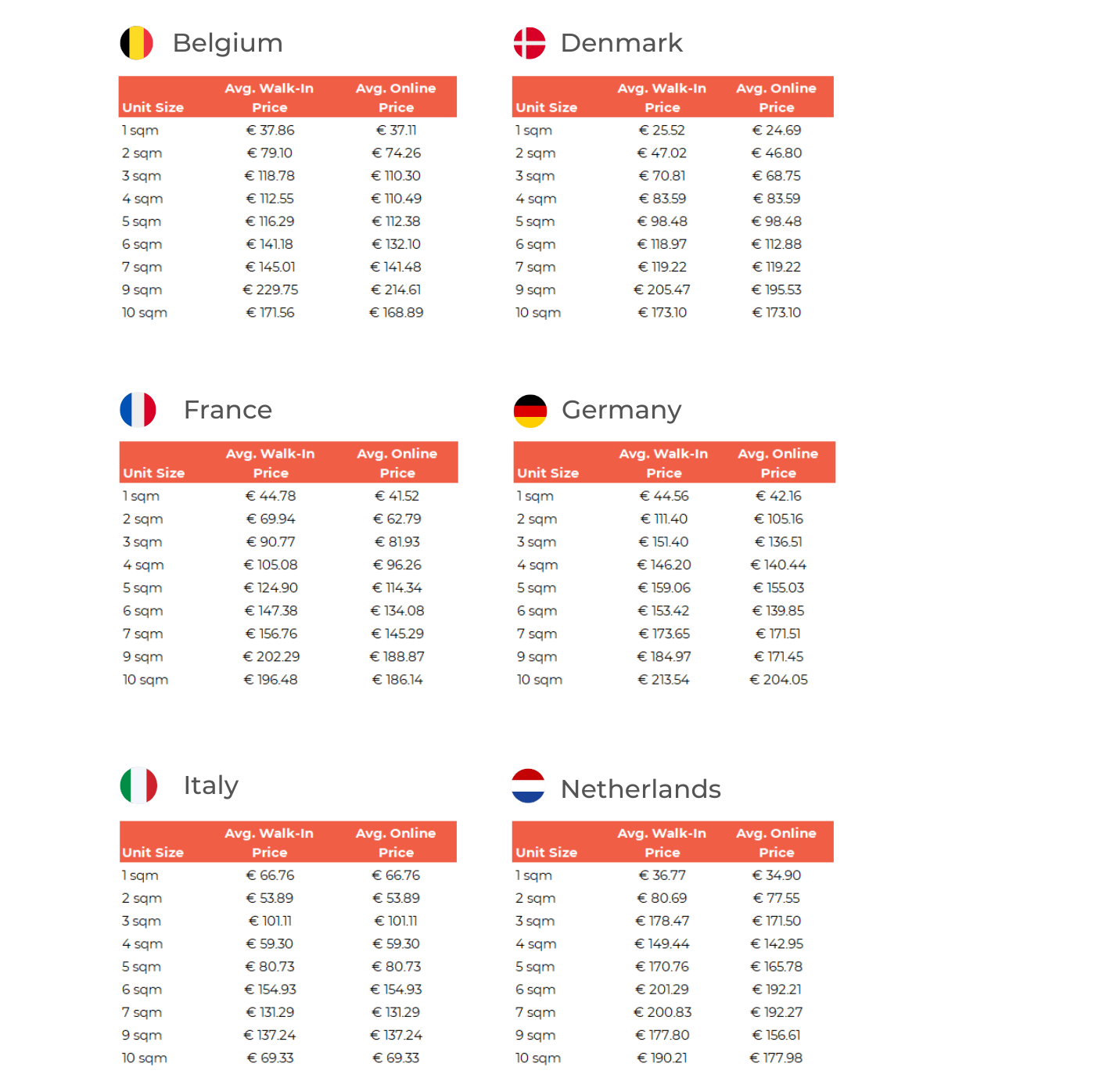

Across continental Europe, supply remains significantly more constrained. France and Germany, two of the region’s largest markets, reported 1,732 and 1,413 facilities, respectively, but with materially lower storage density at just 0.06 sqm per capita in France and 0.04 sqm per capita in Germany, highlighting substantial runway for long-term expansion. Average rates remained elevated across major EU markets, ranging from approximately €23 to €28 in countries such as Belgium, Denmark, France, and Germany, reflecting a combination of limited existing inventory, higher barriers to development, and continued demand concentration in key metro areas.

Europe Market Snapshot

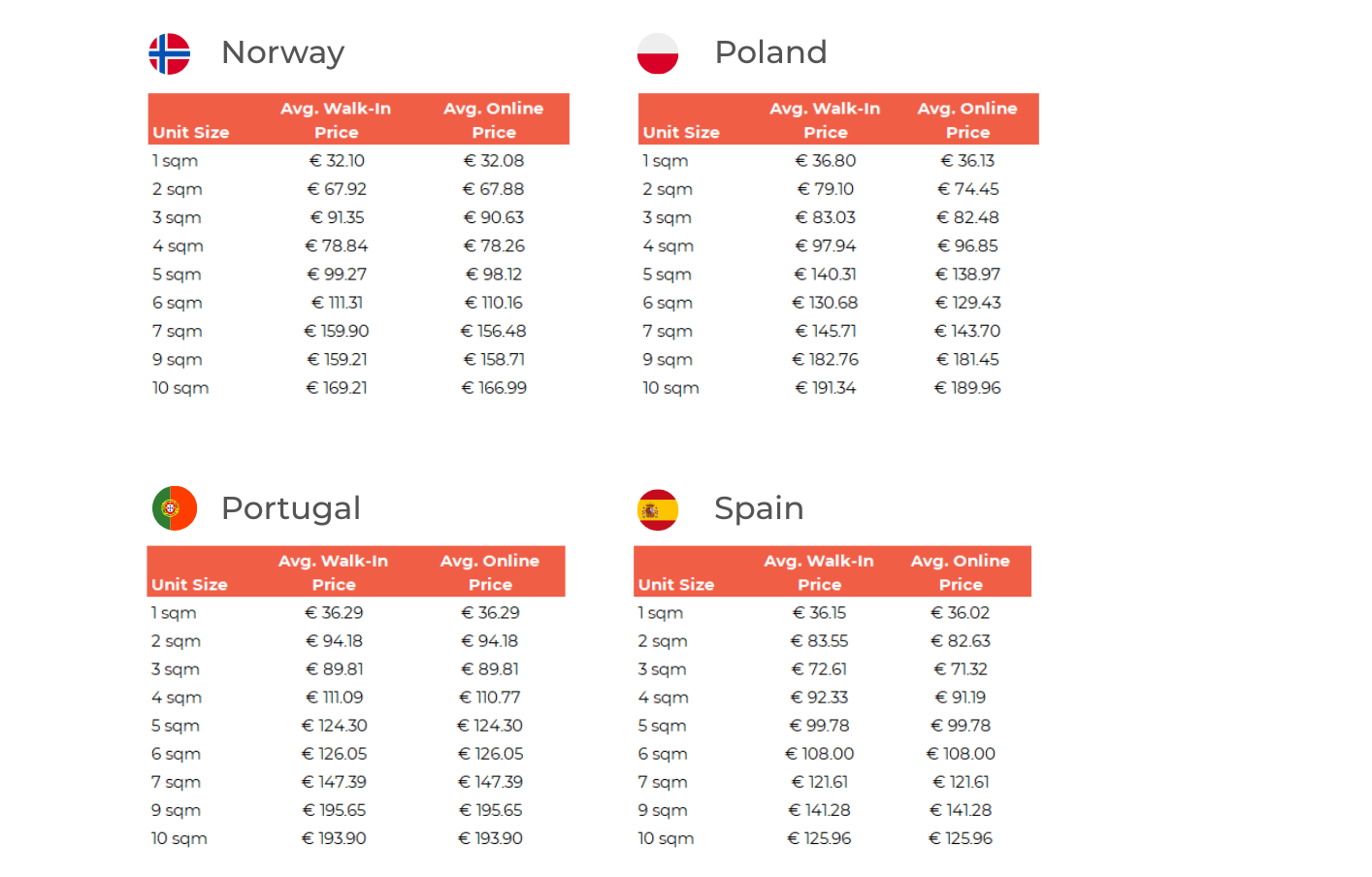

| Country | Net Rentable Space | Total Stores | Population | Supply / capita | Avg. Rate |

|---|---|---|---|---|---|

| UK | 116,298,585 sqft | 5,098 | 67,026,307 | 1.74 sqft | £ 2.64 |

| Belgium | 565,472 sqm | 186 | 11,584,008 | 0.05 sqm | € 23.61 |

| Denmark | 632,222 sqm | 329 | 5,944,145 | 0.11 sqm | € 22.65 |

| France | 3,855,460 sqm | 1,732 | 65,269,154 | 0.06 sqm | € 26.13 |

| Germany | 2,679,627 sqm | 1,413 | 84,358,845 | 0.04 sqm | € 27.84 |

| Italy | 304,314 sqm | 137 | 58,850,717 | 0.005 sqm | € 32.43 |

| Netherlands | 1,961,982 sqm | 816 | 17,590,672 | 0.11 sqm | € 23.46 |

| Norway | 604,242 sqm | 450 | 5,350,859 | 0.11 sqm | € 25.21 |

| Spain | 1,918,808 sqm | 1,444 | 47,539,665 | 0.04 sqm | € 29.59 |

The broader macroeconomic environment also remained a key backdrop. By late 2025, European markets were adjusting to a “higher-for-longer” interest rate cycle, which continued to temper new development activity and place greater emphasis on stabilized assets, operational performance, and disciplined underwriting. At the same time, easing inflation trends and improving consumer sentiment in parts of the region supported steady demand for storage tied to urban mobility, housing transitions, and small business activity. Overall, December pricing and supply dynamics reinforced that while Europe remains structurally undersupplied relative to the UK and U.S., the major EU markets continue to exhibit strong fundamentals and growing institutional relevance heading into 2026.

UK Market

In the UK, December 2025 was headlined by a definitive shift toward institutional consolidation, evidenced by QuadReal Property Group’s £270 million acquisition of the Padlock Euro Storage portfolio. With the market reaching a regionally mature 1.74 square feet per capita across approximately 5,098 facilities, the focus has pivoted from raw development to “flight-to-quality” asset management. While average rates remained high at £2.64, the month was defined by a “yield vs. occupancy” tug-of-war; major REITs leveraged their scale to offset rising operational costs and business rates, while private equity interest intensified. This activity underscores the UK’s status as a liquid, defensive haven for capital, where the primary objective is now portfolio optimization rather than speculative growth.

| Unit Size | England (Walk-In) | England (Online) | N. Ireland (Walk-In) | N. Ireland (Online) | Scotland (Walk-In) | Scotland (Online) | Wales (Walk-In) | Wales (Online) |

|---|---|---|---|---|---|---|---|---|

| 25 | £24.89 | £23.83 | £30.20 | £29.91 | £20.60 | £20.08 | £18.18 | £17.33 |

| 100 | £56.72 | £54.18 | £80.26 | £77.30 | £47.73 | £46.57 | £42.63 | £40.13 |

| 150 | £77.48 | £74.70 | £101.38 | £97.33 | £68.76 | £67.05 | £71.63 | £64.95 |

| 200 | £105.58 | £101.55 | £153.42 | £146.94 | £86.28 | £84.07 | £90.78 | £81.98 |

European Markets

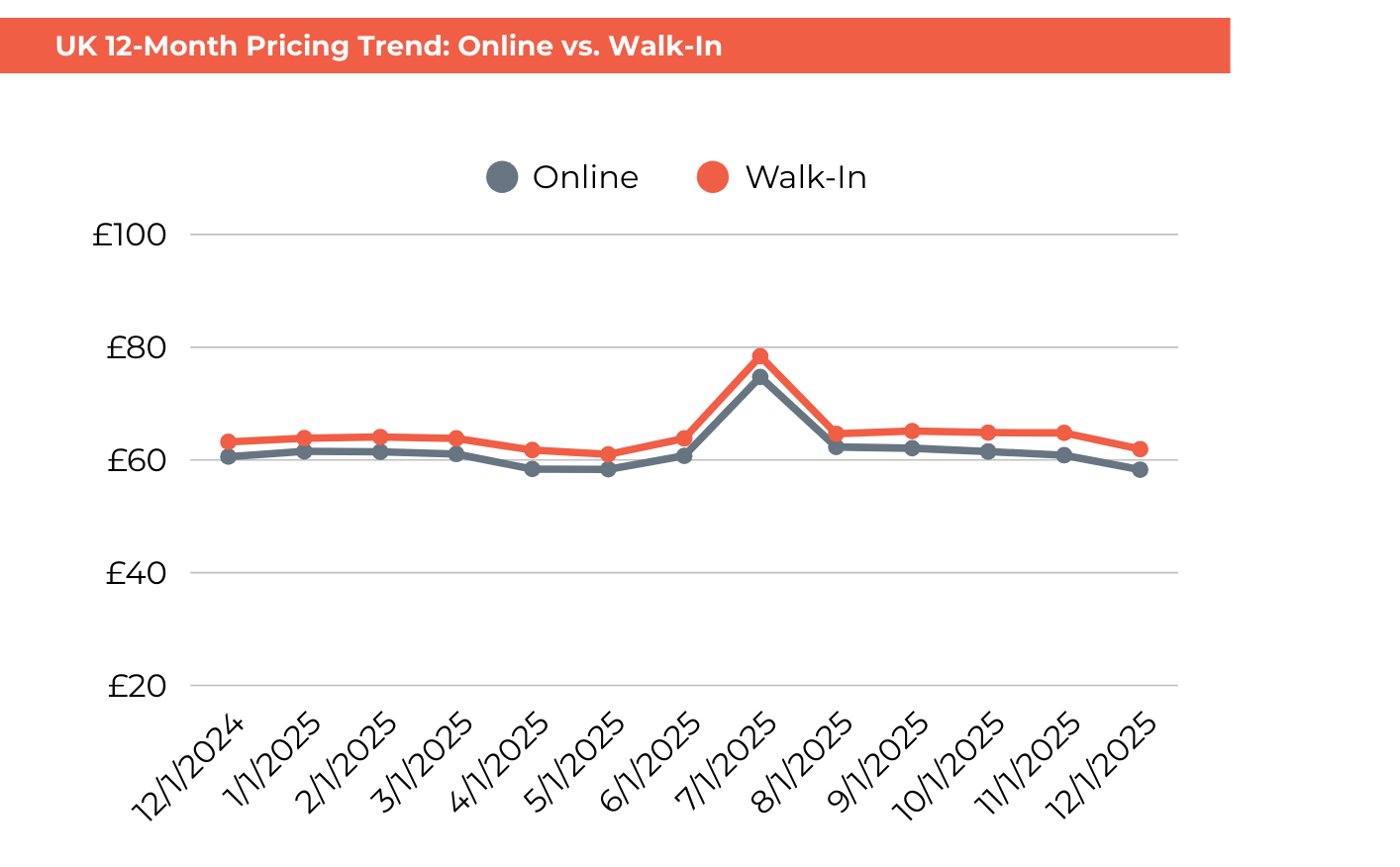

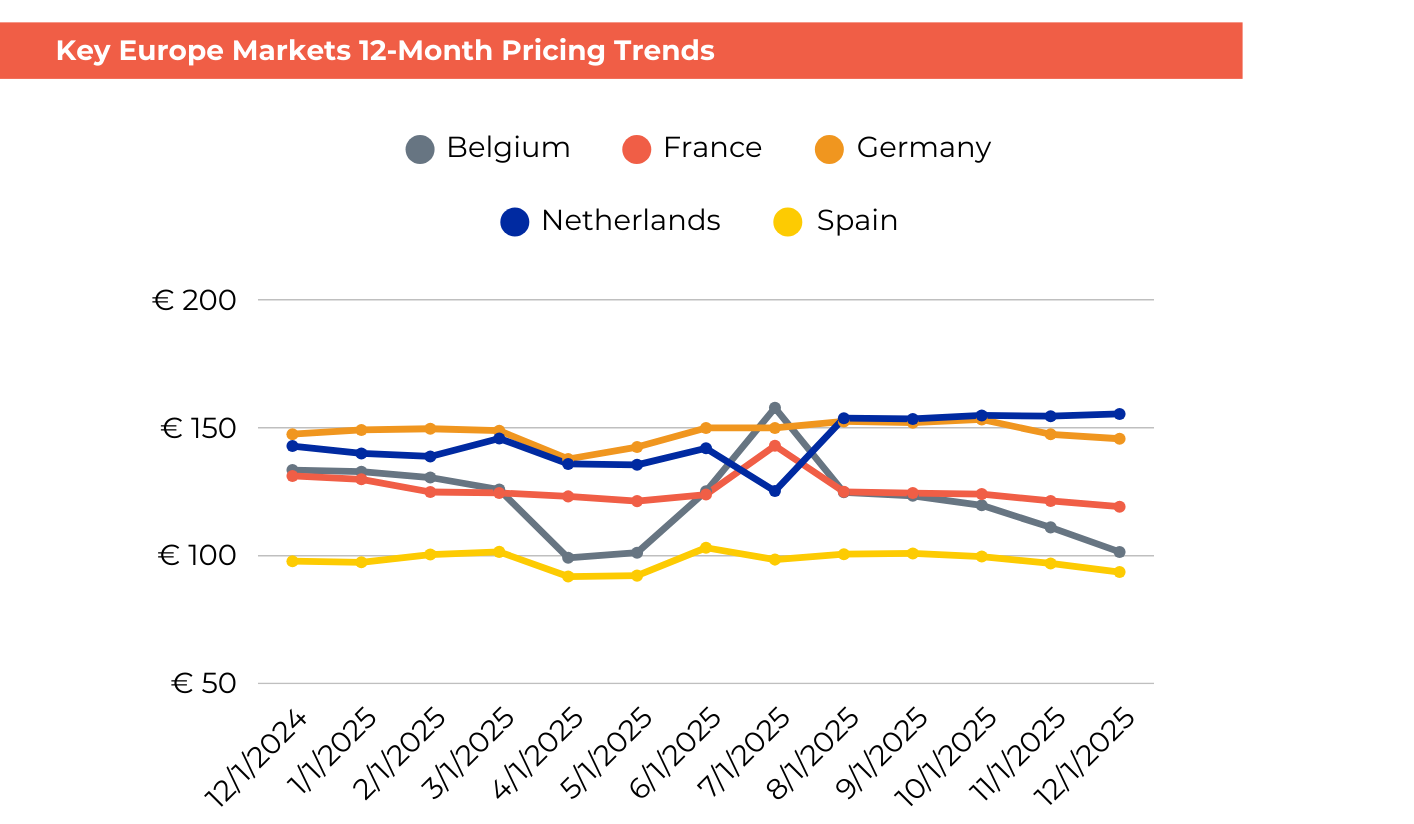

On the European mainland, 2025 was characterized by a “volatility roller coaster” as operators navigated macroeconomic shocks with AI-driven precision. Following a sharp “April Cliff” where rates across the continent plummeted (led by a 21% drop in Belgium) due to trade-related GDP anxiety, the market staged a dramatic mid-summer recovery. July saw massive pricing spikes as high as 26% in key hubs like France and Belgium, capturing peak-season demand. However, the year concluded with a strategic shift toward “occupancy-first” discipline. Supported by significant credit infusions, such as Blackstone’s €100 million loan to Lagerbox, major players in France and Germany prioritized filling their growing pipelines (now totaling over 3,100 facilities combined) over aggressive price hikes. This late-year softening in rates reflects a market maturing into a defensive consolidation phase, prioritizing long-term stability and institutional-grade performance heading into 2026.

Explore Self-Storage Market Dynamics Across the UK & Europe

Access pricing and market intelligence across 20+ European countries. Analyze rates, supply, and competitive positioning in the specific markets that matter most to you.

About StorTrack

StorTrack is the leading authority in self-storage market data and analytics, trusted by operators, investors, developers, and analysts across the globe. Since 2014, StorTrack has delivered the industry’s most comprehensive and accurate insights on pricing, supply, demand, and market trends. Our powerful platforms, Explorer and Optimize, enable data-driven decisions for everything from site selection and feasibility to revenue optimization and competitive benchmarking. With coverage spanning the U.S., Canada, UK, Europe, Australia, and New Zealand, StorTrack empowers professionals to move with confidence in an increasingly complex and competitive landscape. When it comes to self-storage intelligence, data starts here.

The Voice Behind the Data

.jpg)

Christine Wachsman

Director of Market Analytics

Christine Wachsman is the Director of Market Analytics at StorTrack, leading market intelligence across self-storage and outdoor hospitality. As a former economist and lead analyst, she collaborated with institutional and corporate clients. Today, her market insights drive investment strategy across the commercial real estate spectrum, including multifamily, office, industrial, and data centers. She has also served as a panelist and committee member with

organizations focused on advancing real estate analytics and has contributed to industry research and publications.