North America

North America UK

UK Europe

Europe Australia

Australia New Zealand

New ZealandSize, Growth and Key Trends

Understanding the size and scope of a growing, under-penetrated market

The UK self-storage industry is one of the most established and transparent markets in Europe, yet it remains meaningfully underpenetrated by global standards. For operators, investors, and developers evaluating where to deploy capital or expand operations, understanding the true scale and structure of the market is a critical starting point.

This article outlines the key indicators defining the UK self-storage market as of 2026, drawing on StorTrack’s facility-level pricing and market database, which continuously tracks rates, occupancy signals, and supply activity across the country. The analysis covers facility count, total rentable area, per capita supply, pricing benchmarks, occupancy trends, and the development pipeline to provide a comprehensive view of current market conditions.

UK Self-Storage Market At A Glance

- Largest operators: Safestore, Big Yellow Self Storage, Shurgard, Access Self Storage, Storage King

- £1 billion+ in annual revenue, growing at 4–6% per year based on industry estimates

- Average occupancy: approximately 70–90% nationally, based on reporting from major operators with portfolios of 48+ stores

Taken together, these metrics point to a market that is structurally sound, underbuilt relative to demand, and increasingly supported by both data transparency and institutional investment.

Where Are Self-Storage Facilities Located in the UK?

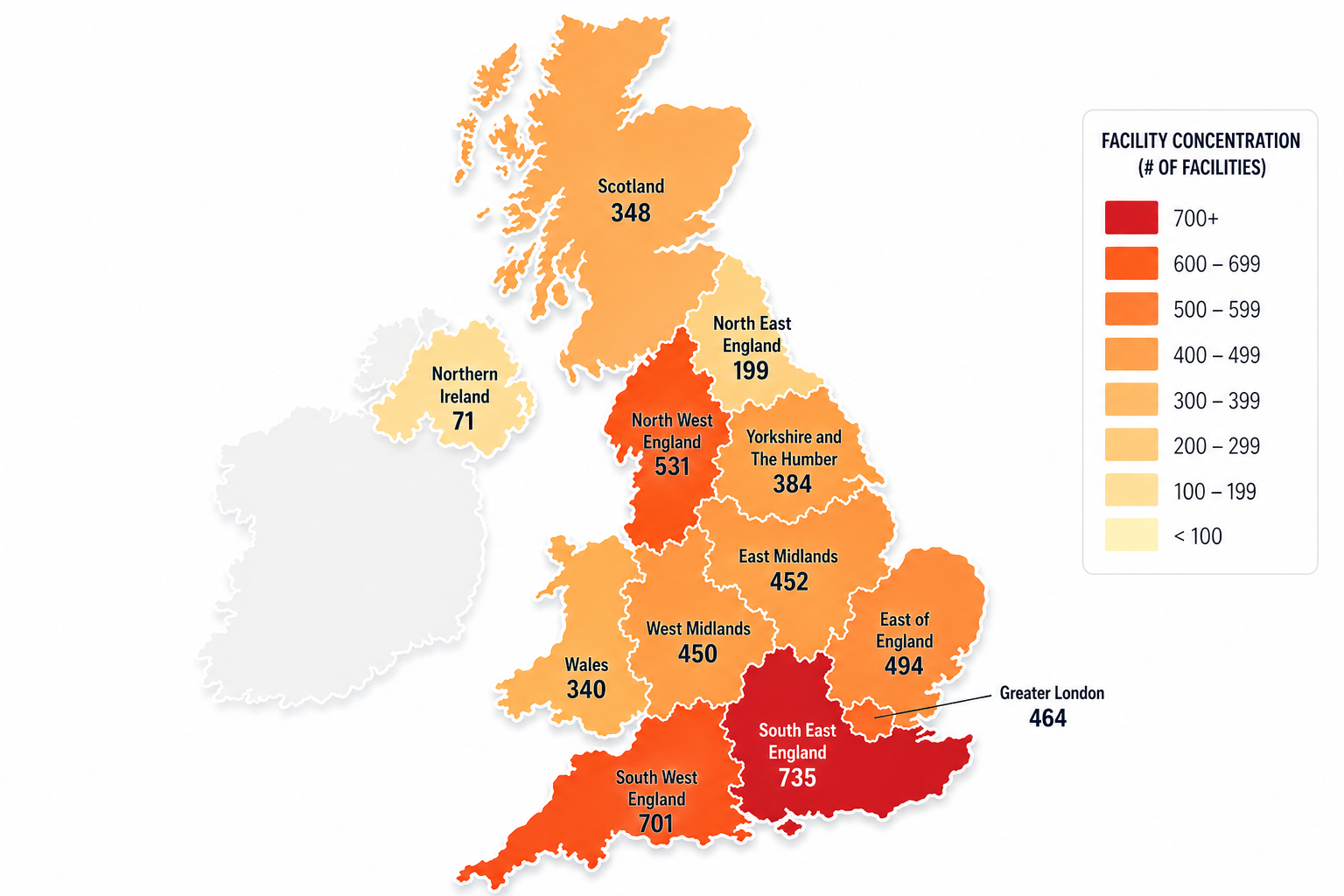

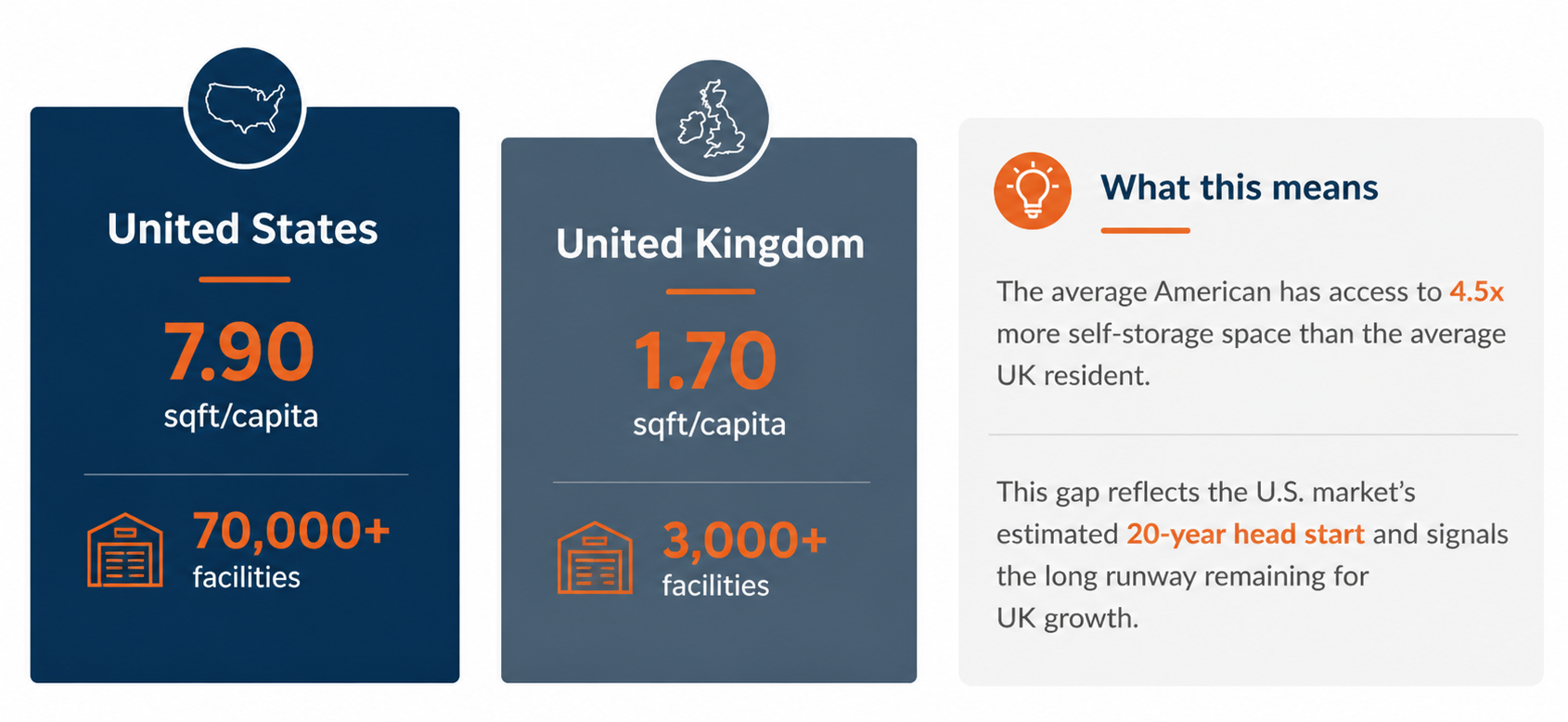

As of 2026, the UK has approximately 5,100 self-storage facilities, making it the largest self-storage market in Europe by facility count, larger than France, Germany, and Spain combined. However, relative to population, it remains significantly smaller than the U.S., which operates over 70,000 facilities serving a population roughly five times larger.

Geographic concentration is a defining feature of the UK market. Greater London and the South account for at least one-third of all facilities, reflecting higher population density, elevated housing costs, and a strong presence of institutional operators.

Beyond the primary regions, several cities, including Manchester, Birmingham, Bristol, Nottingham, and Glasgow, rank among the UK’s largest self-storage submarkets. These markets already operate at a meaningful scale, even as supply per capita remains slightly below the national average.

While not underdeveloped, they have yet to reach the same level of supply density seen in more mature markets. At the same time, select new projects are underway across some of these cities, reflecting continued developer interest. Much of that interest is supported by steady or accelerating population growth, which continues to underpin demand and supports measured expansion over time.

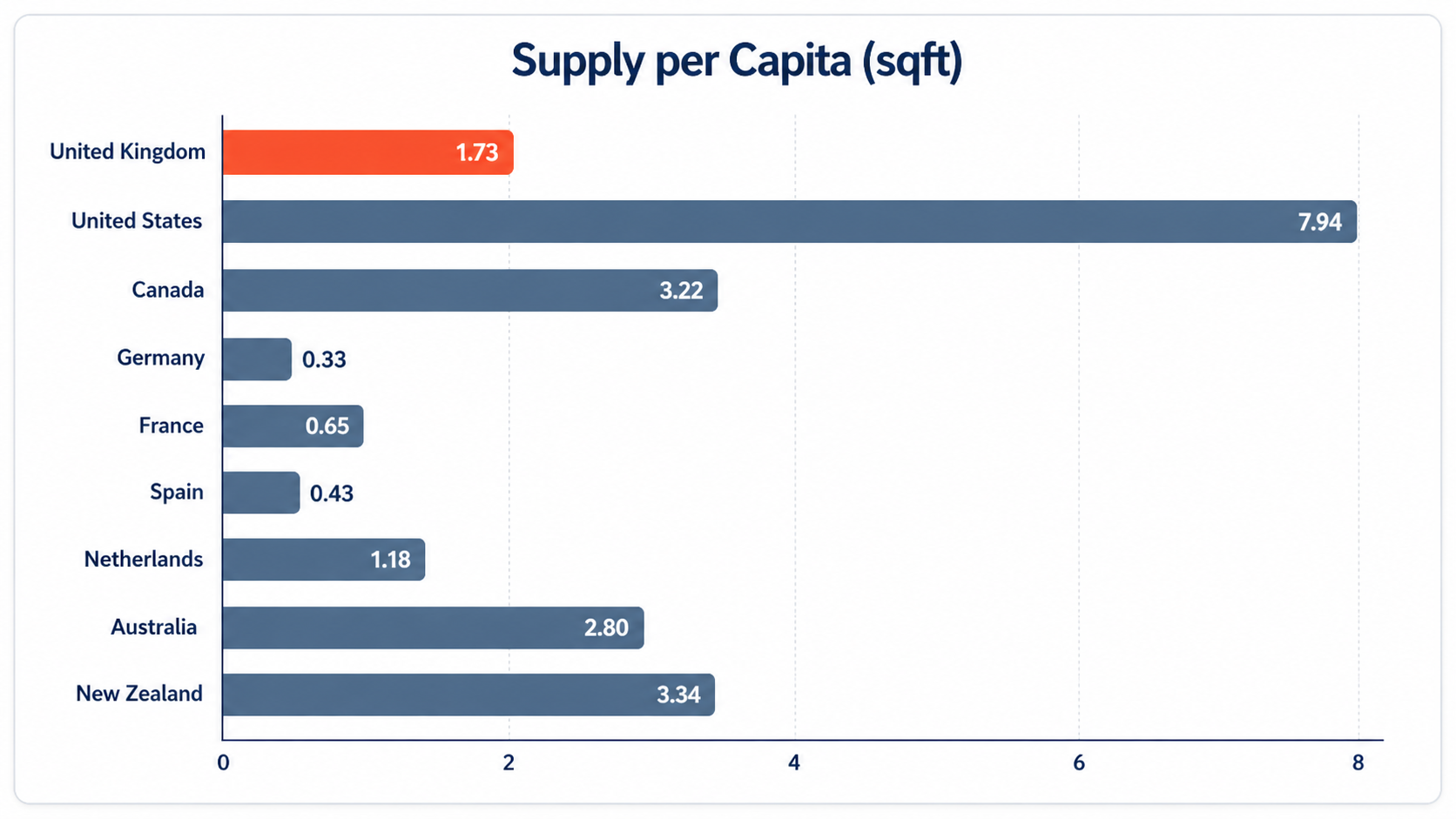

How Does the UK Compare Globally?

With approximately 1.7 square feet of self-storage per capita, the UK sits well below the United States, which averages around 7.9 square feet per capita, and below Australia at roughly 2.8 square feet per capita. Even compared to its closest European peers, the UK’s per capita supply remains low, reinforcing the view that the market has significant structural runway for growth.

While comparisons to the U.S. are frequently cited, they reflect a market that has developed over more than 50 years. A more relevant lens is the UK’s own trajectory, which shows steady expansion driven by urbanization, housing constraints, and increasing business usage. In that context, the UK’s lower per capita supply is less a gap to close immediately and more an indicator of long-term growth potential.

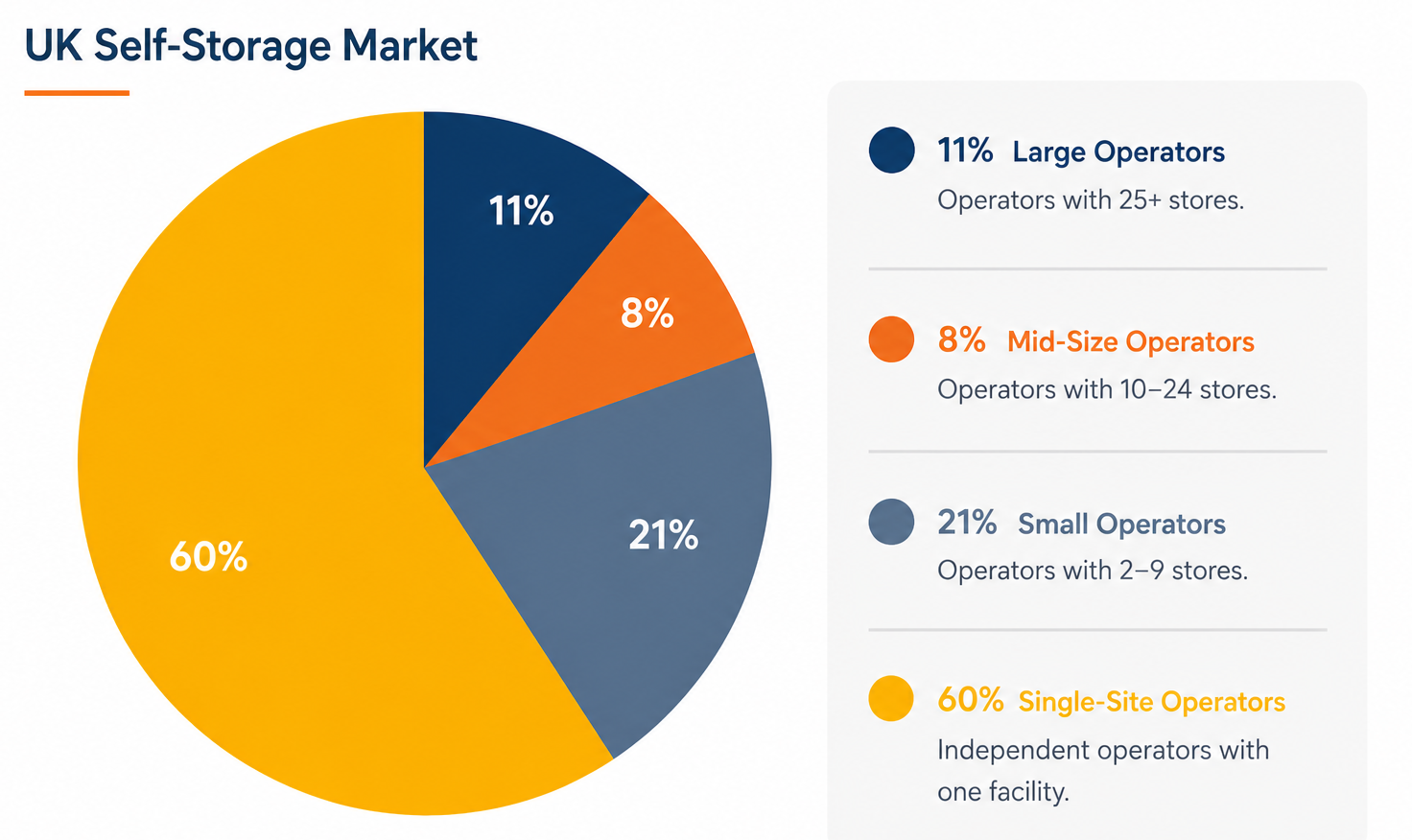

Who Owns and Operates Self-Storage in the UK?

The UK self-storage market is large but remains highly fragmented. While national operators dominate visibility and capital flows, small regional operators and independent owners still account for over 80% of total facilities.

Major operators such as Safestore, Big Yellow, and Shurgard lead in scale and are concentrated in dense urban markets, where barriers to entry are higher and pricing power is stronger. In contrast, mid-sized operators and independents play a more prominent role in suburban and regional markets, where development has historically been more limited and ownership structures more fragmented.

This mix of institutional scale and local ownership continues to shape both competitive dynamics and investment opportunities across the market.

How Much Does Self-Storage Cost in the UK?

As of 2026, average self-storage pricing in the UK is approximately £0.66 per square foot per week, or £34 per square foot per year. However, pricing varies significantly by location, with London submarkets averaging closer to £88 per square foot per year, reflecting higher land costs, stronger demand density, and greater barriers to new supply.

This pricing spread highlights the importance of local market dynamics, where factors such as population density, income levels, and supply constraints can materially influence achievable rates and overall asset performance.

Why Demand for Self-Storage in the UK Continues to Grow

Demand for self-storage in the UK is supported by a combination of structural housing trends, evolving business needs, and relatively low market penetration.

Life transitions

Moving house remains the primary trigger, accounting for approximately 40% of domestic usage, with events such as downsizing, separation, and bereavement also contributing to demand.

Housing constraints

High property prices, smaller living spaces, and limited housing turnover continue to push households toward off-site storage.

Business and SME usage

Approximately 25–30% of customers use storage for business purposes, with SMEs and e-commerce operators relying on it as a flexible alternative to traditional industrial space.

E-commerce growth

Online retailers and micro-fulfilment users represent one of the fastest-growing customer segments.

Low market penetration: Only around 2–3% of the UK population currently uses self-storage, highlighting a significant gap between awareness and adoption.

Together, these factors create a demand base that is both diverse and resilient, supporting steady growth across both consumer and commercial segments.

Industry Revenue and Growth Trajectory

The UK self-storage market now generates over £1 billion in annual revenue, with steady growth of 4–6% per year over the past five years. This momentum is driven by a combination of acute housing market constraints, the expansion of e-commerce and SME operations, and evolving life transitions that necessitate flexible, off-site space.

Key Takeaways

- 5,100+ facilities, making the UK the largest self-storage market in Europe by facility count, yet still early in its development relative to global benchmarks

- 116 million sqft of net rentable area, or 1.70 sqft per capita, highlighting a clear gap between existing supply and long-term demand compared to more mature markets like the U.S. and Australia

- £1 billion+ in annual revenue, growing at 4–6% annually, supported by steady consumer and business demand and a structurally constrained supply environment

- £34/sqft average annual pricing, with higher rates achieved in more supply-constrained submarkets, reinforcing the importance of local market dynamics

- A market still evolving, where growth is being driven not just by new development, but by increasing institutional participation, expanding business usage, and continued rollout across regional cities and surrounding corridors

Ultimately, these dynamics position the UK as a market defined not just by its current size, but by the imbalance between supply and demand that continues to create opportunity for both investors and developers.