Market Overview

Expanding Footprint, Evolving Opportunity

Europe’s self-storage industry is entering a new chapter. No longer a fragmented niche, but a vital and fast-maturing segment of the real estate landscape. With over 13,500 facilities now operating across the continent and annual investment volumes exceeding $1 billion, the sector has moved well beyond its early pioneers.

Amid global uncertainty, European consumer sentiment has remained comparatively steady. According to McKinsey & Company, spending intent rose modestly in the second quarter of 2025, despite U.S. consumers becoming more pessimistic following tariff announcements. Inflation has also eased across most major markets, with OECD data showing an average decline of 65 basis points since the start of the year, though Nordic countries saw a slight increase.

Demand remains underpinned by powerful demographic and behavioral trends. With nearly 70 percent of the global population expected to reside in urban areas by 2050, according to the United Nations, the demand for flexible storage solutions is expected to increase. E-commerce, remote work, and downsizing have also given rise to a “storage economy,” where individuals and businesses increasingly seek secure and scalable storage space.

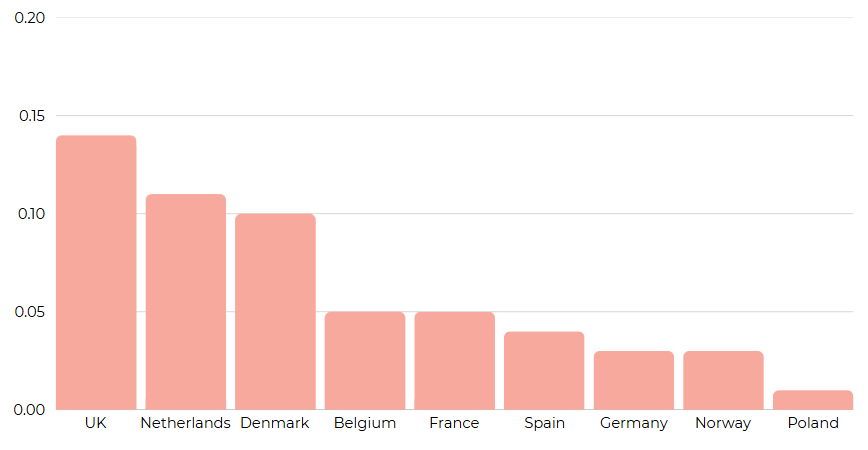

Self-Storage Supply by Market (sqm/capita)

The United Kingdom remains the anchor of the European market, home to 5,233 facilities, nearly 40 percent of the region’s total supply. It also leads in storage density, with 0.14 square meters per capita, more than double the European average. This reflects both a mature consumer market and sustained institutional investment, led by operators such as Shurgard, Safestore, and Big Yellow Group.

On the continent, markets such as Germany, France, and Spain are still in the early phases of adoption, with per capita supply ranging from 0.03 to 0.05 square meters. Yet the fundamentals are in place for continued growth. Urbanization, lifestyle shifts, and digital retail are driving demand, while emerging markets, including Belgium, the Netherlands, Norway, and Poland, are experiencing rapid expansion. Much of this momentum is being fueled by cross-border investors and established platforms.

Once considered a peripheral asset class, self-storage is now firmly on the radar of institutional capital, supported by long-term structural shifts, growing consumer awareness, and a clear need for space in an increasingly compressed urban environment.

Rent Trends

Pricing Stability & Emerging Momentum

Over the past year, self-storage rents across Europe have demonstrated notable stability, even as broader real estate sectors continue to face pricing pressures and economic uncertainty. While short-term fluctuations remain, often tied to seasonality or local supply dynamics, the broader trend reflects strong demand fundamentals and rising consumer familiarity with the product.

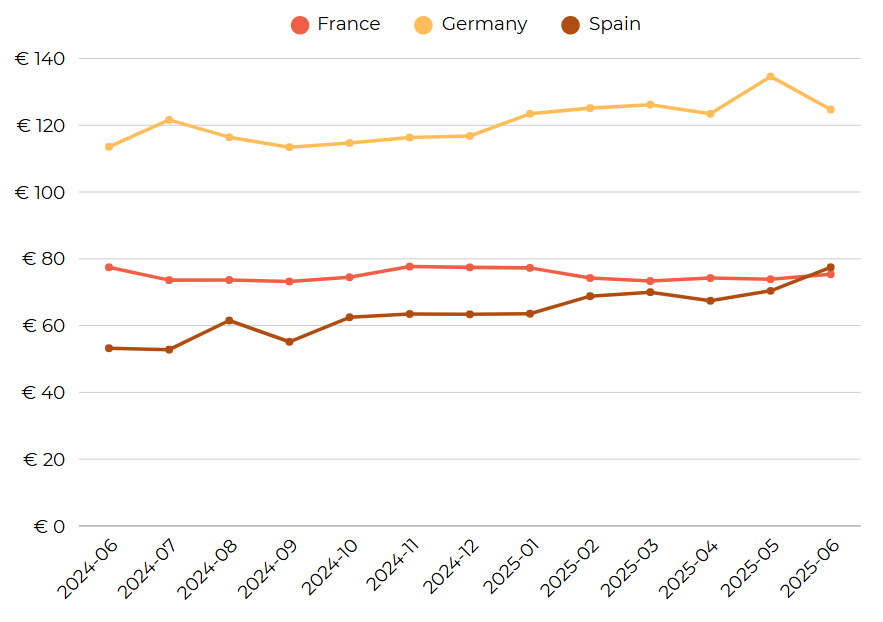

In continental Europe, Germany and Spain recorded modest rent increases, supported by sustained demand growth and measured new development. France, however, remained largely flat. This may reflect a more fragmented competitive landscape, slower consumer uptake, or cautious pricing strategies amid regional economic headwinds. Still, each market continues to demonstrate steady progress and underlying resilience.

Continental Europe (€/sqm)

This graph shows rent trends for benchmark units* only, tracking monthly averages in Germany, France, and Spain over the past 12 months. Each market reflects a distinct stage of evolution within Europe’s self-storage landscape.

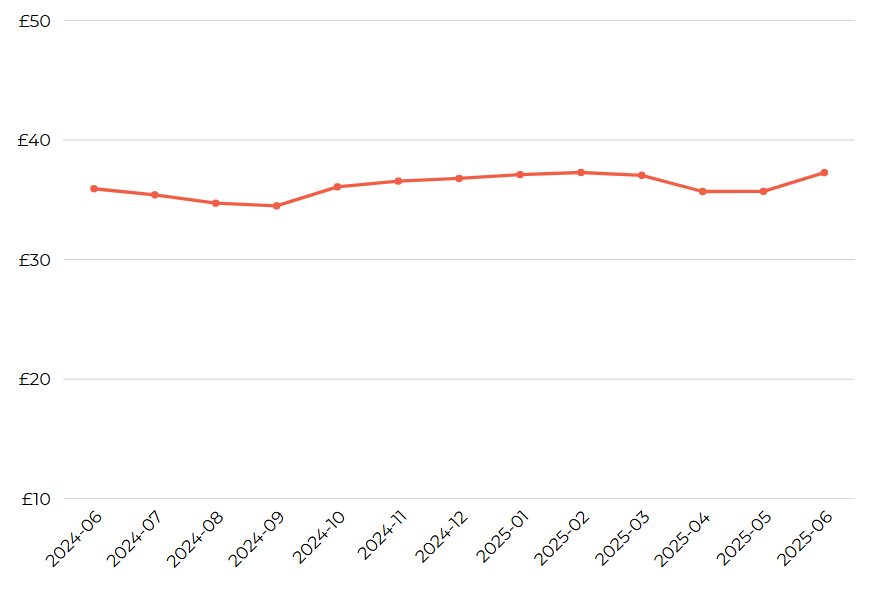

The United Kingdom continues to command the highest rents in Europe, driven by land scarcity, strong urban demand, and an advanced pricing infrastructure shaped by REITs and institutional operators. The consistency of UK rent performance reflects both market maturity and the disciplined application of revenue management tools.

United Kingdom (£/sq ft)

Also based on benchmark units, this graph highlights rent performance in the UK, the region’s most mature self-storage market.

Meanwhile, smaller markets such as Belgium and Norway, although limited in total supply, have exhibited more pronounced seasonal variability. These fluctuations likely stem from weather-dependent leasing patterns, fragmented operator presence, and emerging consumer familiarity.

Together, these trends underscore a sector that is both stabilizing and expanding. Mature markets signal pricing resilience, while emerging ones offer compelling growth trajectories. Amid broader macroeconomic shifts, self-storage remains a demand-driven, opportunity-rich asset class.

Development Trends

From Core Markets to Continental Reach

On the development front, the pipeline across Europe remains active, with most new projects concentrated in and around urban cores. While the United Kingdom, France, Germany, and Spain still lead in total inventory, the 2025 development landscape reveals a broader geographical shift.

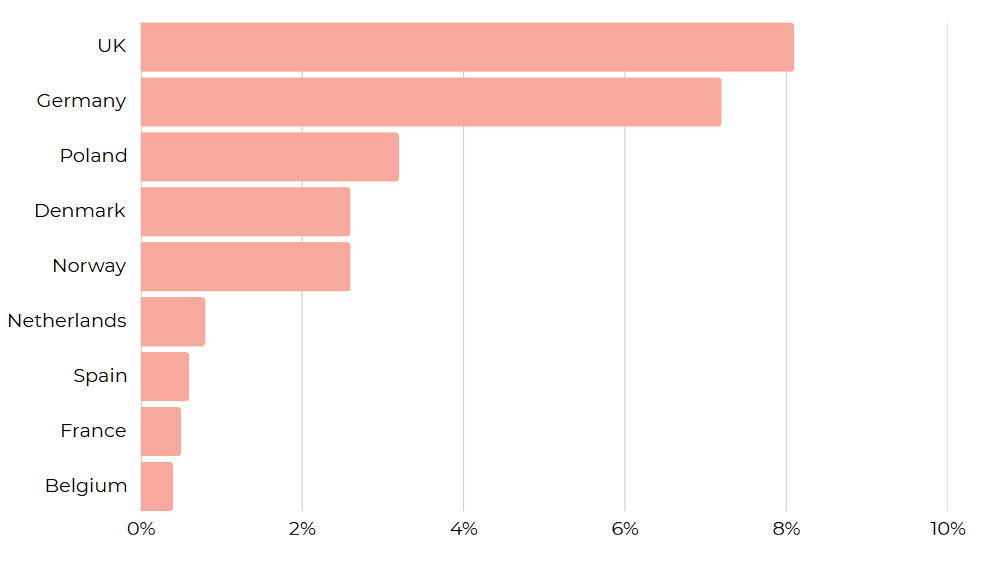

Self-Storage Supply Expansion by Market (%), 2025

This bar graph illustrates the percentage increase in supply across key European markets, based on publicly available data and StorTrack’s proprietary research. It reflects both planned development and active expansion through acquisitions and new builds.

The UK and Germany continue to see robust pipeline activity, driven by sustained urban migration and growing demand from small and medium-sized enterprises (SMEs). At the same time, Poland, Norway, and Denmark are each expanding their self-storage footprint by an estimated 2.5% to 3.5%, underscoring their emergence as growth-oriented markets with rising investor interest.

In Southern Europe, Portugal and Italy are also gaining traction. Growth here is driven by a combination of demographic shifts, constrained urban housing, and increased foreign capital investment. Meanwhile, Poland and the Nordic countries stand out for their low market penetration, increasing urbanization, and the strategic interest they’re attracting from cross-border operators.

This geographic diversification marks a shift in strategy for many leading operators. No longer focused solely on metro dominance, they are now pursuing broader network resilience, balancing urban hubs with regional expansion to capture a wider range of demand drivers and strengthen long-term scale across diverse market conditions.

Capital in Motion

Scaling Europe’s Self-Storage Platforms

As traditional real estate sectors continue to grapple with structural headwinds, investor appetite is increasingly tilting toward alternatives that offer resilient cash flow and operational leverage. Self-storage, alongside sectors like student housing and data centers, has emerged as a top target for capital reallocation. According to Deloitte, platforms that combine stable demand with operational efficiency are now capturing a greater share of institutional portfolios.

This redirection of capital is accelerating both geographic expansion and platform consolidation across Europe. Rather than simply chasing yield, investors are prioritizing scale, infrastructure, and the ability to standardize operations across borders. In doing so, they are helping transform self-storage from a fragmented asset class into a mature, institutional-grade sector.

Institutional Moves Reshaping the Market

The first half of 2025 has underscored this momentum, with a flurry of cross-border acquisitions, joint ventures, and platform-building activity:

- Heitman acquired Servistore, bringing 31 Swedish sites under its platform and establishing a foothold in Scandinavia.

- Harrison Street and Pacific Investments announced a £150M joint venture, targeting the UK’s fast-growing regional markets.

- HESTA, Australia’s AUD 93 billion pension fund, added European self-storage to its alternative property portfolio via Heitman.

- Safestore grew aggressively, executing three joint ventures: Easybox in Italy, myStorage in Germany, and M3 in the Netherlands.

- Shurgard expanded to 318 sites, completing major acquisitions and new builds across Cologne, Paris, and the Benelux region.

These moves reflect more than capital flows; they signal the evolution of self-storage into a full-fledged ecosystem, where technology integration, ESG alignment, and operational agility are increasingly central to investor and operator strategies. With recurring revenue, strong customer retention, and relatively low capex requirements, the business model continues to appeal to institutional capital seeking stability in an otherwise volatile environment.

Outlook

A Defining Inflection Point

As Europe’s self-storage market continues to mature, the focus is shifting from opportunistic growth to strategic scaling. The second half of 2025 is poised to bring further consolidation, rising institutional capital flows, and increasing platform sophistication.

- Urban pricing strength will persist, but operators must navigate zoning, labor, and regulatory constraints.

- Emerging markets, especially in Eastern and Southern Europe, will remain hotbeds for new supply and first-mover advantage.

- ESG standards and automated access systems will become more central to underwriting and consumer decision-making.

- Rising interest from pensions and sovereign capital reflects a broader redefinition of storage as not just a niche solution but a core infrastructure asset in the new economy.

With inflation easing and household incomes remaining steady, Europeans have maintained consistent spending and savings patterns. This economic stability, coupled with growing housing affordability challenges, creates a meaningful open for self-storage to meet evolving space needs.

In an era defined by demographic shifts, urbanization, and technological disruption, self-storage has emerged as a uniquely resilient asset class. What was once a fragmented landscape is transforming into a connected, institutional-grade network, anchored by solid fundamentals and expanding demand across urban and regional markets.

For investors, operators, and developers, the path forward demands strategic clarity: knowing where to scale, how to operate, and when to differentiate.

Key Takeaways

Demand Drivers & Strategic Shifts

- Urban micro-living, aging populations, and e-commerce micro-fulfillment are fueling self-storage usage.

- Business storage is growing at ~7.5% CAGR; climate-controlled units are expanding even faster at ~9% CAGR.

- Digital transformation—online booking, smart access, and usage tracking—is reshaping expectations and competition.

Regional & Segment Highlights

- The U.K. leads Europe’s market with 34–39% of revenue in 2024, followed by Germany and France.

- Spain is the fastest-growing market, projected at ~8.3% CAGR through 2030.

- While personal usage holds ~70% share, business usage is accelerating—creating opportunity for dual-branding and logistics services.

Operational & Investor Strategy

- Operators are shifting from aggressive expansion to prioritizing revenue optimization, occupancy, and selective growth.

- Emerging strategies include hybrid leasing models, structured ECRIs (existing customer rate increases), and tech-enabled pricing to navigate demand.

* StorTrack considers the following unit sizes as benchmark units: 1 sqm, 2sqm, 3 sqm, 4 sqm, 5 sqm, 6 sqm, 7 sqm, 9 sqm, and 10 sqm These unit types are representative of the most common configurations offered across facilities and provide a consistent basis for comparing pricing and availability between markets.

About StorTrack

StorTrack is the leading authority in self-storage market data and analytics, trusted by operators, investors, developers, and analysts across the globe. Since 2014, StorTrack has delivered the industry’s most comprehensive and accurate insights on pricing, supply, demand, and market trends. Our powerful platforms—Explorer and Optimize—enable data-driven decisions for everything from site selection and feasibility to revenue optimization and competitive benchmarking. With coverage spanning the U.S., Canada, UK, Europe, Australia, and New Zealand, StorTrack empowers professionals to move with confidence in an increasingly complex and competitive landscape. When it comes to self-storage intelligence, data starts here.

Need deeper insights or custom reports?