July 8, 2025

Navigating a Crossroads in Self-Storage

The self-storage sector has reached a pivotal point in its post-pandemic evolution. Following several years of demand-driven growth, the market began to recalibrate in 2024 amid rising economic uncertainty, shifting consumer sentiment, and persistently elevated interest rates. These factors prompted a reassessment of expectations across the industry. By early 2025, however, emerging indicators point to signs of stabilization, with operators beginning to adjust strategies in response to the new landscape.

2024: The Year of Reset

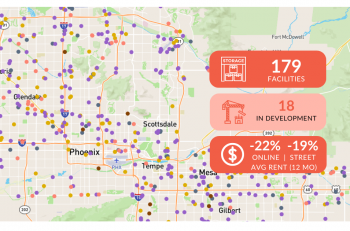

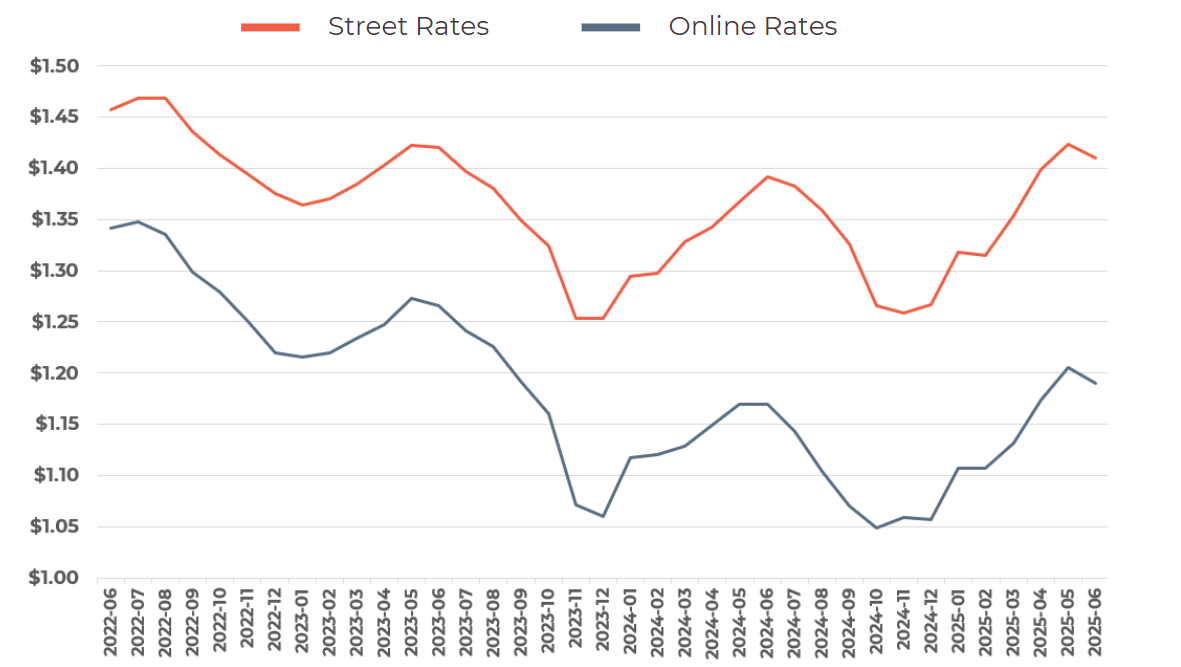

The national average for self-storage street rents declined 2.5% in 2024 as the industry adjusted to tighter financing, slower residential mobility, and cooling consumer confidence. Leasing activity slowed as home sales hit a lull, and operators turned to aggressive promotional pricing to protect occupancy. The gap between online rates and street rates widened to 19% at its peak, eating into margins and placing further pressure on revenue growth.

Street vs. Online Rates: 3-Year Trend

But the story wasn’t all contraction. Supply pipelines decelerated as construction costs remained high and lending conditions tightened. This supply-side pause provided some relief in saturated metros, and forward-thinking operators focused on tenant retention, operational efficiency, and localized pricing strategies.

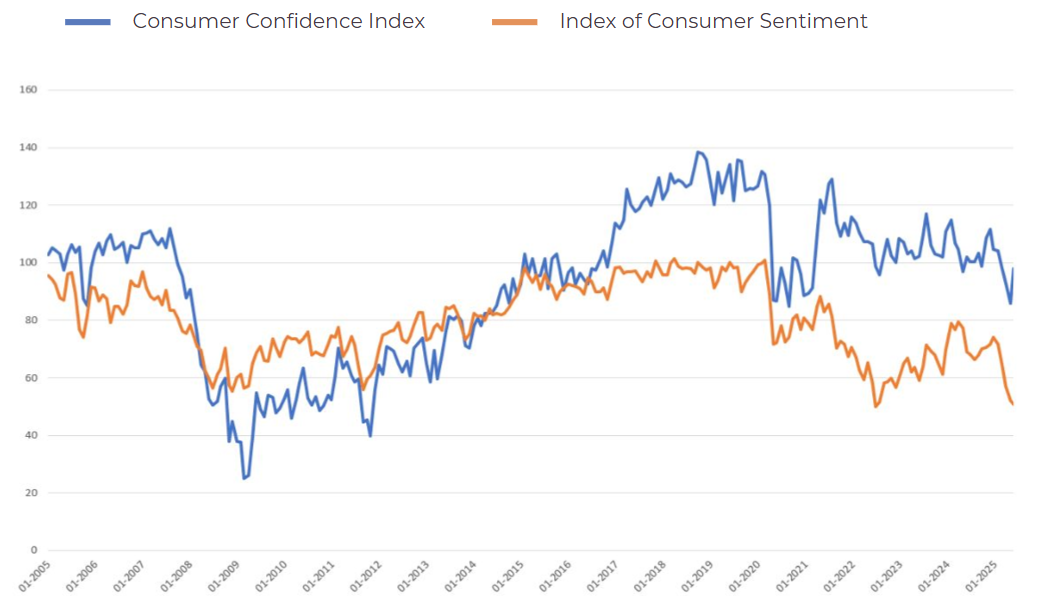

Consumer sentiment remained cautious but showed tentative signs of recovery. In May 2025, the Conference Board’s Consumer Confidence Index edged up to 98.0, halting a five-month decline. In contrast, the University of Michigan’s Sentiment Index slipped to 50.8, underscoring continued financial strain across households. Taken together, these signals highlight that self-storage demand is driven more by life transitions – death, divorce, downsizing, dislocation – than by discretionary spending. Even during periods of economic uncertainty, the underlying need for space proves resilient.

Consumer Confidence vs. Sentiment (2005-2025)

Index Base = 100

Data Source: University of Michigan and The Conference Board

First Half of 2025: Signals of Stabilization

In the first half of 2025 (1H 2025) the sector hit what appears to be a pricing floor. National average rents turned modestly positive, climbing 1.3% year-over-year compared to last year’s 2% YoY decline. That spike was modest but meaningful.

Even more promising: the gap between online and street rates narrowed from 19% to 16%, suggesting renewed pricing discipline. An uptick in digital traffic and a slowdown in move-in declines contributed to improved month-over-month performance among REITs. Occupancy levels began to stabilize, while dynamic pricing tools allowed operators to adapt more swiftly to shifting demand.

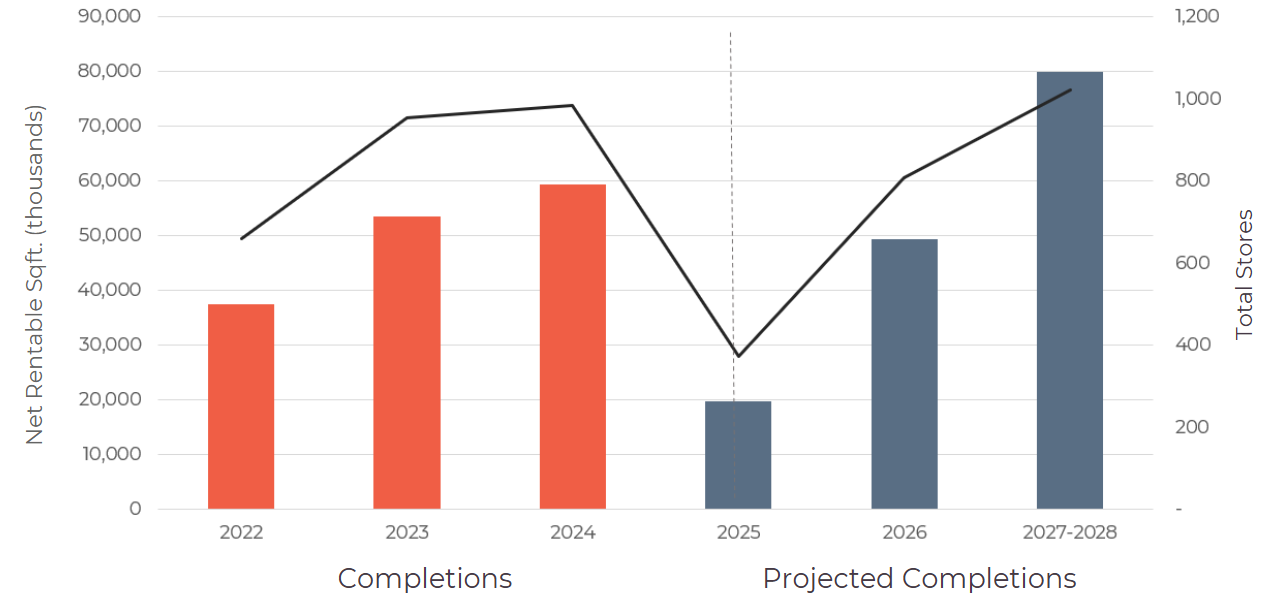

As for new supply, while concerns about oversaturation persist in many key markets, continued population growth and solid long-term demand fundamentals are keeping developers optimistic despite short-term macro headwinds. Development activity has slowed notably due to rising supply costs, driven by tariffs and continued labor shortages. Only about 20 million rentable square feet (373 projects) are expected to be delivered in 2025, a sharp drop from 2024’s 59 million rentable square feet (985 projects) in completions. Nevertheless, over the next two to three years, StorTrack data shows nearly $2 billion worth or projects are in the pipeline, including those already under construction and others in the final planning stages.

Development Pipeline

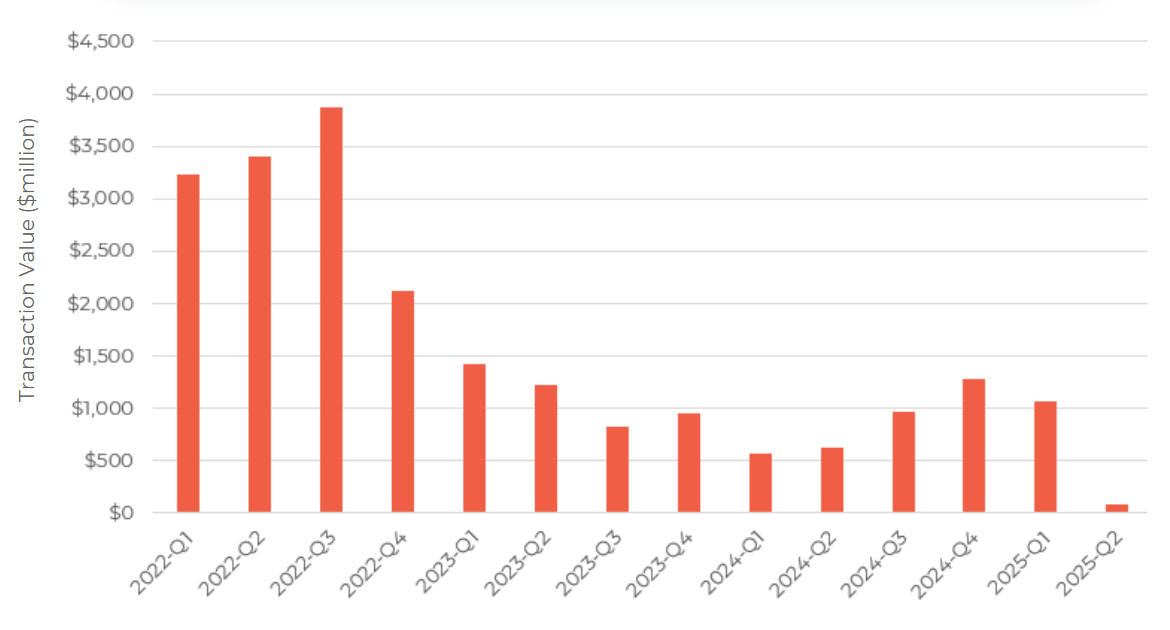

While new development has slowed, investment activity in H1 2025 is shaping up to be a promising counterpoint, reflecting continued confidence in the sector. The first quarter saw over a $1 billion in closed deals, down slightly from the prior quarter’s $1.28 billion – the highest since Q1 2023 – yet, still signaling resilient investor interest. Early transaction data for Q2, with $88 million recorded so far, suggests momentum could build further, putting the market on track to surpass H1 2024’s performance.

U.S. Self-Storage Deal Volume by Quarter

Regional Divergence and Localized Drivers

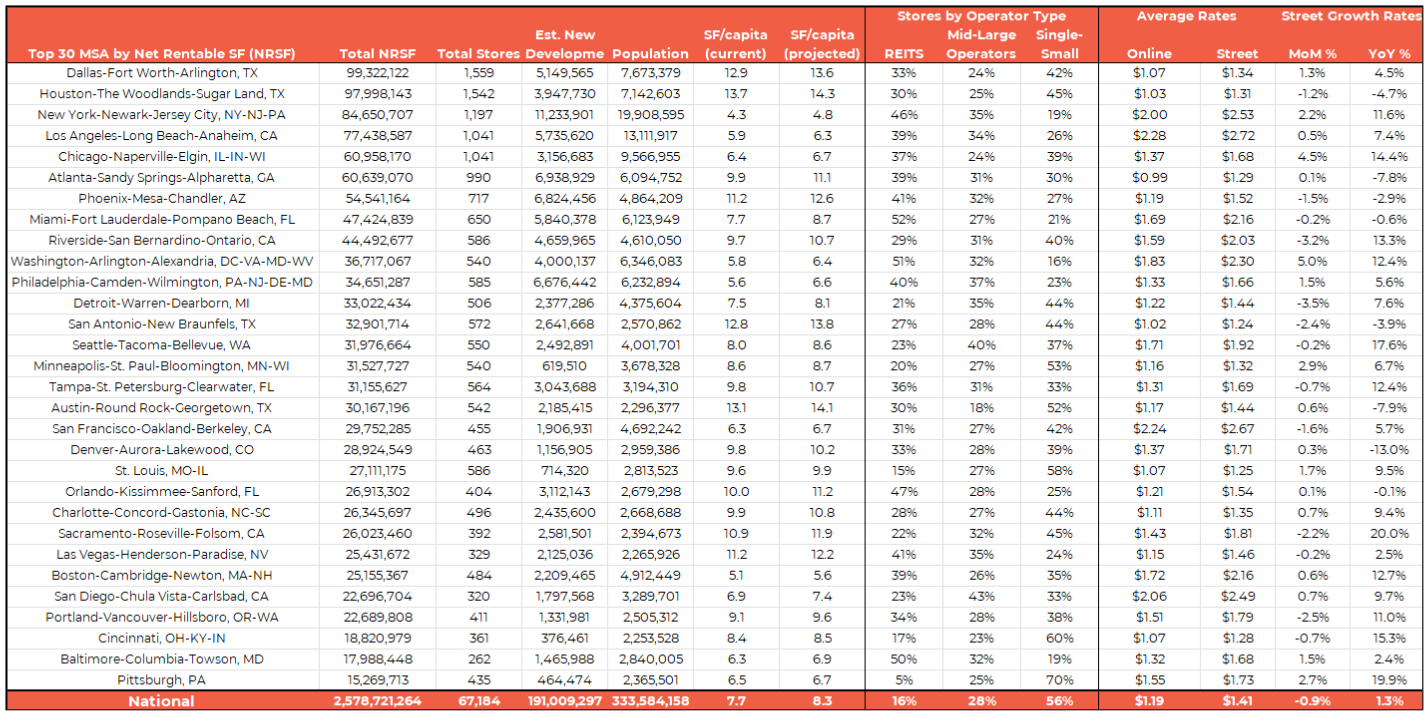

Market performance has grown increasingly uneven across regions, shaped less by broad national trends and more by localized supply-demand dynamics.

Top Performers

Washington, D.C. led with 15.4% rent growth over three months and 12% year-over-year gains, supported by only 5.8 sf/capita. Chicago followed with 14.4% annual growth, also bolstered by sub-average supply (6.4 sf/capita).

Gateway Strength

New York and Los Angeles remain pricing leaders, with average rents above $2.50/sf despite limited new supply. New York grew 11.6% YoY, and L.A. posted 7% gains.

Growth Corridors

Sacramento, Pittsburgh, Seattle, and Riverside-San Bernardino all posted double-digit rent growth despite diverse supply profiles, suggesting regional migration and local demographics are at play.

Lagging Markets

Denver (-13%), Austin (-8%), and Atlanta (-8%) experienced YoY declines, often tied to oversupply and slower absorption. The Southwest overall underperformed, with four of five markets showing rent drops amid oversupply of 11+ sf/capita.

Southeast Caution

Despite rapid population growth, Miami and Orlando posted flat rents and continued to build aggressively, with 12%+ pipelines. Dallas saw modest 4.5% growth, but supply remains a watch point at 10+ sf/capita.

In total, 20 of the top 30 MSAs saw rent growth between 2.5% and 20% year-over-year. The remaining 10 experienced negative performance, highlighting a widening performance gap and reinforcing the need for localized strategy.

REITs: Market Movers in a Maturing Cycle

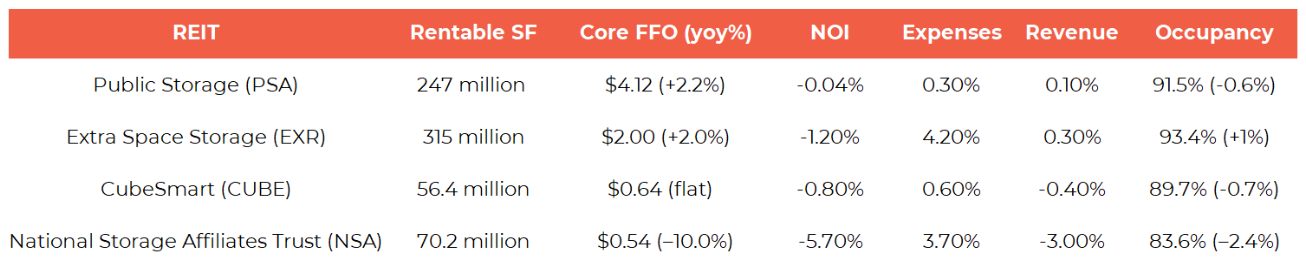

![]() Public REITs continue to set the tone for the self-storage sector. As the industry’s largest owners, developers, and capital allocators, their strategic decisions shape broader market behavior, from pricing expectations to transaction activity and development trends. In the current environment, REITs have pivoted from rapid expansion to operational optimization. The focus has shifted to sustaining occupancy, optimizing revenue, and recalibrating growth for a more selective cycle. Despite persistent macroeconomic headwinds, early 2025 performance points to emerging signs of portfolio stabilization.

Public REITs continue to set the tone for the self-storage sector. As the industry’s largest owners, developers, and capital allocators, their strategic decisions shape broader market behavior, from pricing expectations to transaction activity and development trends. In the current environment, REITs have pivoted from rapid expansion to operational optimization. The focus has shifted to sustaining occupancy, optimizing revenue, and recalibrating growth for a more selective cycle. Despite persistent macroeconomic headwinds, early 2025 performance points to emerging signs of portfolio stabilization.

CubeSmart (CUBE)

Narrowed move-in declines from -10% to just -2% and FFO remained flat despite a modest dip in occupancy to 89.7%. These results reflect disciplined operations and early signs of demand stabilization. The company continued its expanding its footprint, particularly in high-barrier-to-entry markets like New York, balancing growth with a focus on core performance.

Extra Space Storage (EXR)

Reported 93.7% occupancy and stabilized street rates in Q1 2025. Core FFO rose 2% year-over-year, supported by disciplined revenue management and ongoing integration of the Life Storage portfolio. The company expanded its footprint with 12 acquisitions and the addition of over 100 facilities to its third-party management platform, signaling a continued focus on balanced growth and operational efficiency amid a more selective investment environment.

Public Storage (PSA)

Posted positive move-in trends and a narrowing occupancy gap in early 2025. Core FFO declined largely due to FX losses, partially offset by NOI gains. Higher property taxes drove operating costs, though lower payroll expenses provided relief. The REIT acquired at least nine properties and has over 3.5 million rentable square feet under development, reflecting a measured but ongoing growth strategy. Foot traffic remained above 2024 levels and was up 2% compared to Q1 2019 (a key pre-pandemic baseline), indicating sustained consumer demand.

National Storage Affiliates Trust (NSAT)

Delivered the softest performance among peers, with a 5.7% decline in same-store NOI and occupancy at 83.6% in Q1 2025. Despite near-term headwinds, NSAT remains focused on disciplined growth, acquiring three facilities in Q1 and continuing to prioritize self-storage assets with the top 100 MSAs.

What unites all five is a decisive shift away from speculative building. Development starts have slowed significantly, with capital redirected toward infill conversions, stabilized asset acquisitions, and revenue optimization. REITs are also leading the charge on technology-driven pricing, customer service innovation, and digital marketing efficiency, creating performance gaps between institutional-grade operators and independent owners.

As interest rates and cap rates remain elevated, REITs are using their scale and balance sheets to stay ahead. Their next moves will likely define the tempo of the market through 2025 and shape which metros see renewed investment and which remain in pause mode.

Economic Headwinds Still Matter

Tariff announcements, geopolitical tensions, and a volatile bond market have kept economic uncertainty front and center. While mortgage rates dipped early in 2025, they have since hovered near 7% in response to U.S. trade policy changes, causing home sales to stall. This “pause” in the housing market continues to limit self-storage move-ins tied to housing transitions. Still, unemployment remains low, and economic fundamentals are holding. If housing activity resumes later in 2025, storage demand could see another tailwind.

What’s Next: A More Disciplined Growth Phase

The rest of 2025 will likely be defined by selective growth and sharper market segmentation. Operators who adapt pricing strategies, leverage local data, and right-size their unit mixes will lead performance as national averages give way to metro-level variation.

Markets like Charlotte, Tampa, and Boise, with low per-capita supply and strong population growth, are showing early pricing power. Meanwhile, capital is flowing toward high-occupancy, stabilized assets in metros with clear demand fundamentals and limited new supply.

The boom years may be over, but self-storage continues to show resilience and operational depth. The next wave of growth will come not from momentum but from precision.

StorTrack is the leading authority in self-storage market data and analytics, trusted by operators, investors, developers, and analysts across the globe. Since 2014, StorTrack has delivered the industry’s most comprehensive and accurate insights on pricing, supply, demand, and market trends. Our powerful platforms—Explorer and Optimize—enable data-driven decisions for everything from site selection and feasibility to revenue optimization and competitive benchmarking. With coverage spanning the U.S., Canada, UK, Europe, Australia, and New Zealand, StorTrack empowers professionals to move with confidence in an increasingly complex and competitive landscape. When it comes to self-storage intelligence, data starts here.

![]()